From February 25th 2025 - Making America Healthy Again by Empowering Patients with Clear, Accurate, and Actionable Healthcare Pricing Information;

From April 15th 2025 – Lowering Drug Prices by Once Again Putting Americans First;

From May 5th, 2025 – Regulatory Relief to Promote Domestic Production of Critical Medications;

From May 12th, 2025 – Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients

targeting healthcare price transparency, drug pricing, and domestic pharmaceutical production created a complex landscape for originator (brand-name) and generic drug manufacturers, both domestic and foreign. These policies aim to reduce U.S. drug prices, incentivize domestic manufacturing, and balance global pricing disparities favoring US patients.

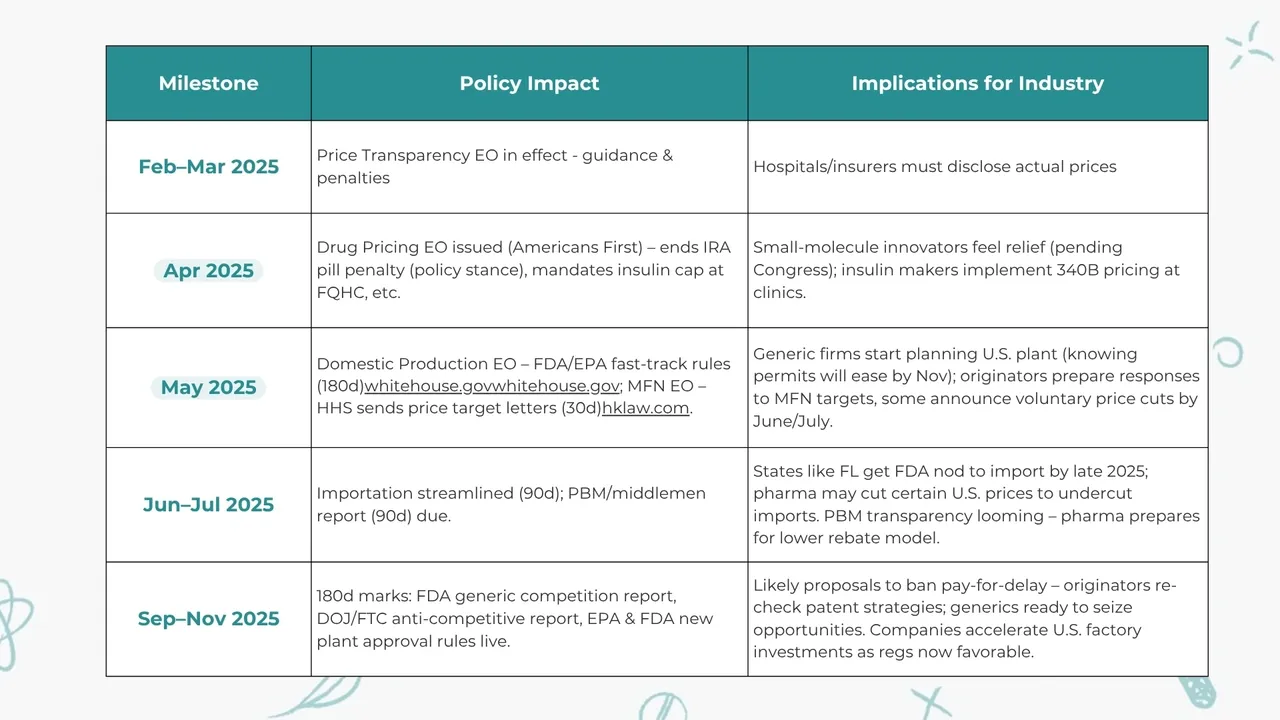

Here is a brief timeline table:

.webp)

An obvious goal of the strategy and Eos is that the distinction between domestic and foreign companies will be more: domestic firms, whether brand or generic, should leverage their home advantage – engaging with government initiatives, highlighting U.S. investments, and benefiting from smoother regulatory pathways. Foreign firms will have to mitigate their “outsider” risk by localizing operations, aligning with U.S. policy goals (for instance, offering key drugs at reasonable prices in the U.S. market voluntarily), and demonstrating their contributions to U.S. health (such as through reliable supply or innovative therapies).

From a strategic business development director’s lens, these changes open up new partnering opportunities: collaborations between big pharma and generics for authorized generics or biosimilars, joint ventures to produce drugs domestically, technology tie-ups to upgrade manufacturing, and data-sharing partnerships to prove value. We are likely to see more cross-sector alliances – for example, pharma companies partnering with insurers or pharmacy chains to implement direct sales or value-based pilots. Companies that historically operated in silos will have stimulus to engage more with the broader healthcare system to adapt their business models. The EOs and the strategy is enforcing changes across the value chain:

Here is another table with impact by industry:

My wild guess is that altogether these stakeholders represent over US $3 trillion in equity value—and their strategic responses will determine how quickly the EOs will deliver lower costs, expanded manufacturing, and new licensing opportunities.

The market is expected to shift: U.S. drug spending growth may temper as prices come down, but volume could increase if more patients can afford treatments. Generic utilization could rise further and with new biosimilars and import options, payers will have more tools to manage costs. Industry consolidation is a possibility – weaker players (especially those unable to cope with new cost structures or compliance standards) might exit or merge, while strong, adaptive players will grow. We may also see consolidation in the generic industry accelerate. Smaller generic companies might sell their ANDAs or merge to handle the costs. A more consolidated generic industry might paradoxically have more pricing power in some niches, but the Administration’s competition focus will discourage any anti-competitive consolidations. Commercially, generics could try to enter more specialty areas (complex generics, biosimilars) where profits remain despite general pricing pressure. Additionally, to consolidation and genericalizaiton of the market, I would like to underline elimination of the “Pill Penalty” – a notable change in the April 2025 drug pricing EO aligning negotiation timing for small-molecule drugs with biologics. Under current law, Medicare price negotiation can hit small-molecule drugs 9 years after approval versus 13 years for biologics. This so-called “pill penalty” has been criticized for skewing toward biologics at the expense of traditional drugs for larger populations. The EO effectively promises originator companies a longer protected revenue window for pills, assuming legislative change. This is a clear win for small-molecule innovations.

The timeline of impacts suggests that the next 2–3 years are critical for strategic repositioning. By 2028, many of these policies will likely be entrenched, and companies that adopt the changes early will be in a stronger position than those that resisted.

In conclusion, the combined impact of the 2025 EOs will be a more transparent, more competitive, and more domestically anchored U.S. pharmaceutical market. Originator companies will likely see narrower international price gaps and must innovate efficiently, but they’ll gain a more sustainable footing with patients and payers if they adapt. Generic companies will become even more crucial, effectively the backbone of an affordable system, and those that invest in quality and supply reliability will thrive. For both, the mantra should be collaboration and adaptation: work with regulators, with healthcare partners, and even with one’s traditional competitors in new ways. By doing so, pharmaceutical companies can turn a challenging regulatory push into an opportunity – to streamline operations, build goodwill, and ultimately reach more patients in need with life-saving therapies at prices society can bear.

Sources: